Buried in the Notes: Where Salmon Farming Earnings Are Really Decided

Most investors read salmon farming annual reports the same way.

They start with the CEO letter, scan the operational review, and anchor on reported earnings. If they go further, they strip out Fair Value adjustments and focus on “underlying” performance.

That approach is logical—and it misses something important.

Because in salmon farming, the most useful information is often not in the narrative.

It’s in the notes.

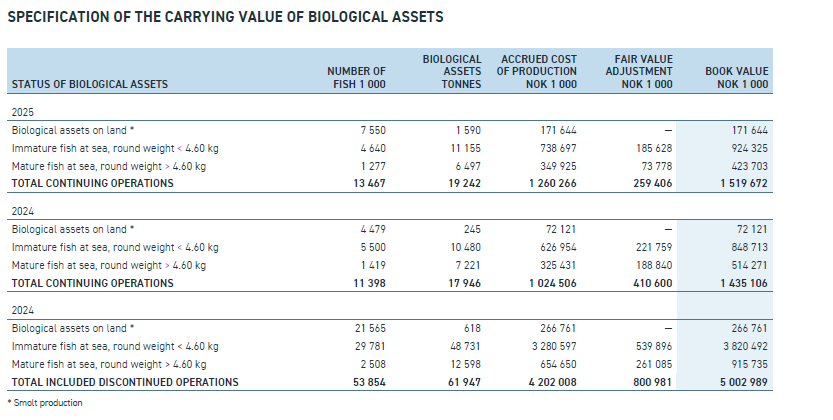

Take Grieg Seafood’s 2025 annual report. The CEO and board commentary discuss biological challenges, cost pressures, and operational performance. The story is clear: a difficult year but broadly understood.

But buried in the Fair Value tables is something much more precise. Based on the disclosed biomass and accumulated cost, the cost of fish still in the water increased from roughly NOK 57/kg to over NOK 65/kg year-on-year—an increase of approximately 15%.

From the Grieg Seafoods 2025 Annual Report - page 123

That number does not appear in the CEO letter.

It does not appear in the board report.

But it is one of the most important numbers in the document.

In salmon farming, earnings are largely determined months before they are reported. Growth rates, mortality, feed conversion, and treatment costs accumulate over a 12–24 month cycle. By the time fish are harvested and sold, much of the economic outcome has already been set.

The question isn’t what the company earned. It’s what the fish are going to earn and that answer is rarely in the headline numbers.

Fair Value has always had an uneasy place in aquaculture reporting. It flows through the income statement, but it isn’t cash. It can distort period-to-period earnings, and the instinct to ignore it—or strip it out—is not wrong.

While the Fair Value adjustment itself can be noisy, the structure behind it is not. It forces companies to reconcile four things: biomass, biological performance, cost to harvest, and expected price.

Those inputs are not theoretical. They are the economic reality of the fish in the water.

What makes this particularly important is the way cost behaves in a biological system.

In most industries, cost is recognized when it is incurred. In salmon farming, a large portion of cost is capitalized into the biomass. Feed, treatments, labour, and time all accumulate inside the fish. That cost base only becomes visible in the income statement when the fish are harvested. Until then, it sits in the water.

Which means that a change in cost structure does not show up immediately in earnings. It shows up first in the Fair Value tables—as a change in the cost of biomass. That is what the 15% increase in Grieg’s cost per kilo is capturing.

Not a forecast.

Not a narrative.

An embedded reality.

Across the industry, this underlying reality is always there—but it isn’t always easy to see.

In some reports, the Fair Value mechanics are explicit. You can see how prices are constructed and how costs are built through to harvest.

In others, the biology is clearer than the valuation—mortality, growth, and disruption are described in detail, but not pulled into a single economic view.

And sometimes, the signal is fragmented. The Fair Value note is high-level, while the most important indicators sit elsewhere in the report.

But the underlying dynamic doesn’t change.

Cost accumulates before revenue is realized.

Biology drives that cost.

And both are visible before they appear in earnings.

For investors, this creates a different way of reading the accounts.

Instead of asking whether Fair Value should be included or excluded from earnings, the more useful question is: What is already embedded in the biomass?

Is the cost base rising or falling?

Is the system becoming more or less efficient?

Are biological conditions improving or deteriorating in ways that will affect future margins?

These are not abstract questions. They are the bridge between current disclosures and future performance.

None of this makes Fair Value easy to work with. It remains imperfect, subjective, and sensitive to assumptions. But dismissing it entirely leaves a gap in understanding—one that matters in a business where the asset is alive, the production cycle is long, and the lag between cause and effect is measured in quarters, not days.

If you want to understand what a salmon farming company has earned, you can start with EBIT.

If you want to understand what it is likely to earn next, you have to go deeper into the document.

That’s where the cost is building.

That’s where the biology shows up.