What China Will Discover About Salmon—Just Like Everyone Else

I was asked this week about the threat China poses to the salmon sector.

The question was framed in familiar terms: cost, speed, and scale. China can build faster. Build cheaper. Deploy infrastructure at a pace that few others can match.

All of that is true.

But it’s not where the outcome is being determined.

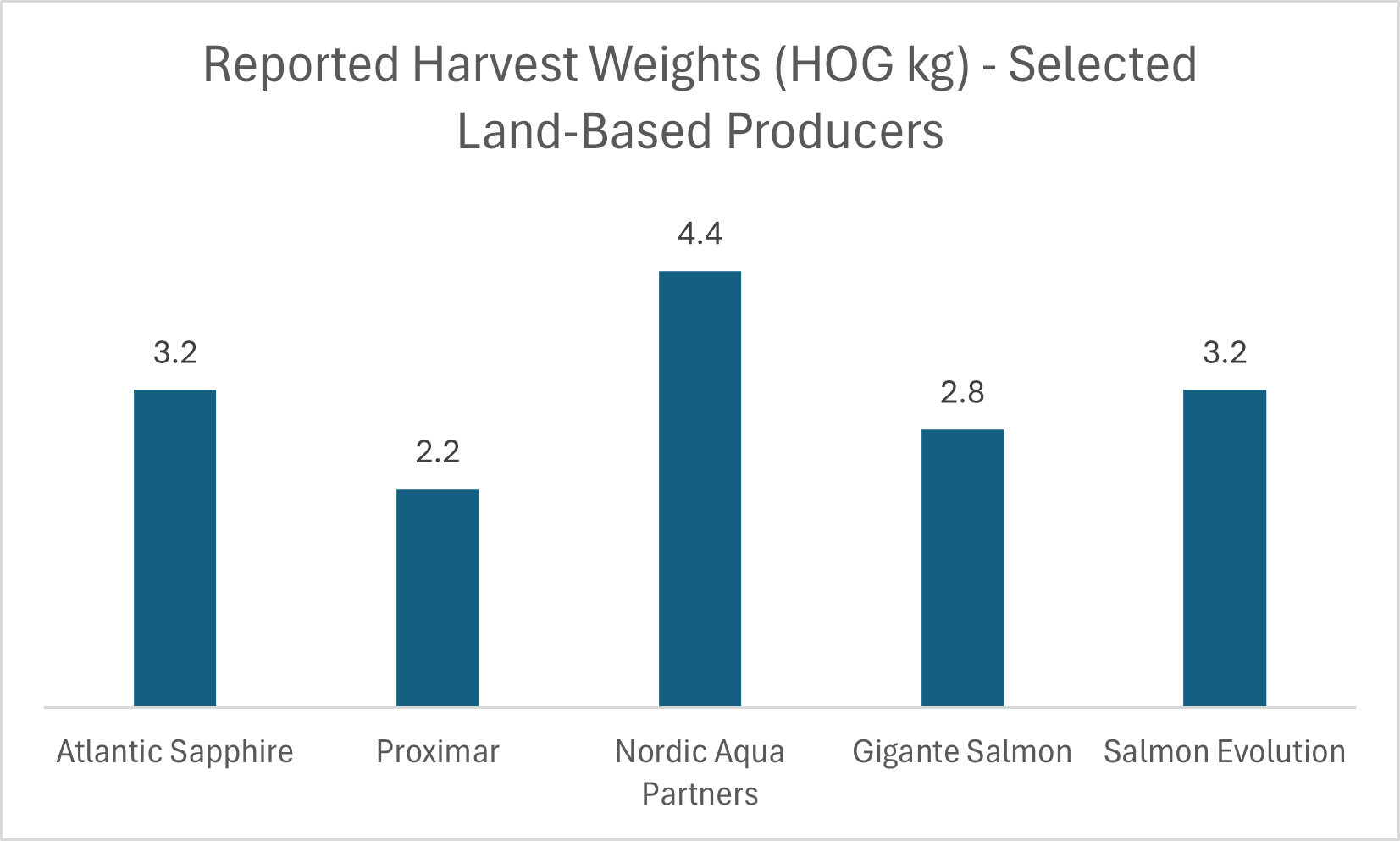

Over the past few weeks, Q1 updates from land-based salmon producers have started to come through. Different geographies. Different systems. Different teams. But the language is remarkably consistent.

Smaller fish.

“Optimizing biomass profiles.”

Clearing production constraints.

Positioning for improved performance in the next cycle.

From Q1 2026 Production Updates - average industry weight for salmon is 4.5 - 5.5 kg HOG

It would be easy to read this as a collection of execution issues. Operators still climbing the learning curve. Early-stage inefficiencies that will be ironed out over time.

That’s not what it is. What we are seeing—repeatedly—is biology asserting itself inside tightly engineered systems. These are not failures of design or intent. They are systems encountering limits.

Land-based salmon farming is often framed as an engineering problem. Control the water. Control the inputs. Stabilize the environment. Remove the variability that defines open systems.

But salmon are not passive components. They carry metabolic constraints that don’t disappear when the system becomes more controlled—if anything, those constraints become more tightly coupled to system performance.

Oxygen demand rises with biomass.

Waste accumulates faster than it can be processed.

Density amplifies stress.

Growth becomes uneven under pressure.

Engineering can shape the environment in which these forces play out. It cannot remove them.

What’s notable is not that these issues are appearing—but where they are appearing.

Many of the operators now reporting these outcomes are not new to salmon farming. They are operating in regions with deep industry experience. They understand the species. They understand the risks.

And still, the systems are settling into a pattern:

Push toward design capacity → encounter constraint → reset biomass → rebuild.

Not a smooth ramp. A negotiated equilibrium.

This is where the conversation about China becomes more interesting.

Because China will almost certainly excel on the engineering side.

They will build systems faster.

They will reduce capital costs.

They will iterate designs quickly and at scale.

What they are not importing along with that infrastructure is decades of accumulated farming craft. And that distinction matters.

Salmon farming is not just a technical process. It is a practiced one.

Knowing when to push biomass—and when not to.

Recognizing early signals of instability.

Managing growth variability before it becomes a system-wide issue.

Balancing production targets against biological tolerance.

These are not embedded in the design. They are learned. The Western industry is still learning them in the context of intensive, land-based systems—often in real time, and at significant cost.

China will be on that same curve.

But there is an important nuance.

They don’t need to be as good as the Norwegians to succeed.

Norwegian producers operate in a global commodity market. Their benchmark is world pricing, shaped by supply from multiple regions and formats. Margins are earned through consistency, scale, and operational precision. China is playing a different game.

Proximity to end markets reduces logistics friction.

Avoidance of airfreight changes the cost structure materially.

Domestic demand provides a degree of insulation from global price dynamics.

That shifts the threshold. The question is not whether China can achieve optimal biological performance.

It’s whether they can achieve sufficient biological performance—at a cost base that still works.

That creates two plausible paths.

In one, they move steadily up the learning curve. They internalize the biological constraints, develop the operational craft, and build a viable domestic industry that doesn’t need to mirror Norwegian performance to be profitable.

In the other, engineering confidence runs ahead of biological understanding. Systems are pushed harder, scaled faster, and operated closer to their limits—producing periods of strong output, followed by the same resets and instability now visible elsewhere.

Neither outcome would be surprising.

For investors, the key point is this:

China is not just a supply story. It is a learning curve—one that is already visible in markets with far more experience.

The Q1 reports are not an anomaly. They are a signal. Not that the model doesn’t work, but that it works within constraints that are still being discovered.

The question is not whether China can build these systems.

It’s whether building them faster accelerates the learning.