How Much Supply Growth Does Salmon Pricing Tolerate?

If salmon demand is truly “price neutral” at 7–8% annual growth, why have prices historically weakened at much lower supply growth levels?

For more than a decade, the salmon industry benefited from a remarkably supportive market structure.

Production growth was constrained by licensing systems, environmental regulation, biological challenges and geographic limitations. At the same time, global demand expanded steadily as salmon established itself as a mainstream premium protein category across retail and foodservice markets.

The result was a powerful scarcity narrative.

Periods of weak biology or operational disruption reinforced the idea that supply growth would remain structurally limited. Strong pricing absorbed rising operating costs, increasingly complex farming practices and steadily growing capital intensity. Existing producers generated record profits while investors increasingly viewed salmon farming as a uniquely attractive combination of biological scarcity and long-term demand growth.

This framework shaped not only how salmon producers were valued, but also how expansion projects were financed.

Many of the large-scale land-based salmon projects developed over the past decade were conceived during this environment. These projects were not financed solely on technological optimism. They were financed on the assumption that structurally unmet demand and robust salmon pricing would persist over long periods of time.

The events of 2025 and early 2026 do not necessarily invalidate this broader scarcity thesis. Salmon supply remains constrained in ways that few other protein industries are. New farming regions remain difficult to develop, biological challenges remain unresolved and land-based production has not materially altered global supply dynamics.

However, the recent market environment may raise an uncomfortable question for investors.

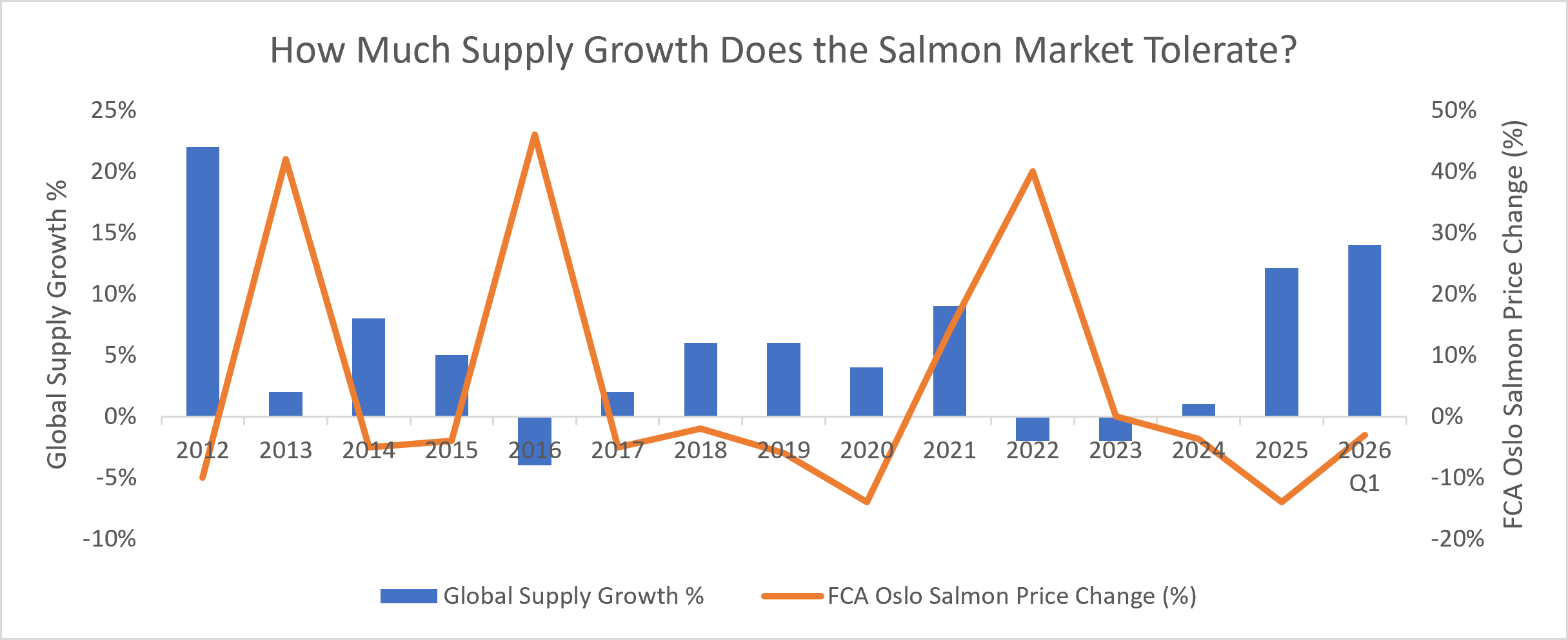

How much supply growth does the salmon market actually tolerate before pricing weakens?

Industry commentary has often referenced long-term demand growth in the range of 7–8% annually. If this assumption broadly holds true, periods of moderate supply growth should theoretically be absorbed without major pricing disruption.

Historically, however, the relationship may not have been quite so forgiving.

Looking back over the past decade, salmon prices have frequently weakened during periods when global supply growth exceeded only modest levels. In many years, supply growth in the range of 4–6% was sufficient to pressure prices meaningfully. The recent experience of 2025 and early 2026 may simply represent a more extreme version of this same dynamic.

This distinction matters because it potentially changes how investors should think about risk within the sector.

The traditional scarcity narrative implicitly encouraged the view that constrained long-term supply growth would naturally support durable pricing power. But if relatively modest increases in harvest volumes are consistently capable of pressuring prices, then the industry may be more cyclical than the long-term narrative sometimes implies.

That does not make salmon farming unattractive. It simply means that pricing behavior may be more sensitive to incremental volume changes than investors became accustomed to during the strongest years of the scarcity cycle.

The implications become particularly important for capital-intensive production systems.

Established producers can often absorb weaker pricing periods through existing operating scale, mature infrastructure and diversified cash flow generation. Early-stage projects, however, are typically most financially exposed precisely when pricing weakens, unit costs remain elevated and financing requirements remain high.

This may be especially relevant for land-based salmon projects.

Many were financed during a period when salmon appeared to operate within a relatively stable equilibrium: constrained supply combined with robust and seemingly durable demand growth. The assumption was not necessarily that prices would rise indefinitely, but that the market would remain structurally tight enough to support attractive long-term economics.

If the market is actually more sensitive to incremental supply growth than many investors assumed, that framework becomes more complicated.

A period of elevated supply growth does not need to permanently undermine salmon pricing to create financial pressure. It simply needs to weaken prices for long enough to challenge projects still climbing the production curve.

For mature producers, this may represent normal cyclical volatility.

For projects dependent on strong pricing assumptions during ramp-up periods, the consequences can be far more significant.

The key question for investors may no longer be whether salmon remains structurally scarce.

The key question may be how much pricing volatility structurally scarce industries can still produce.