The EBITDA Mirage:

What Q3-2025 Revealed About the Economics of Land-Based Salmon Farming

Q3-2025 was an unusually revealing quarter for land-based salmon farmers. Across the sector — Salmon Evolution in Norway, Nordic Aqua Partners in China, Proximar in Japan and others — biological performance improved. Fish were larger, survival was strong, standing biomass increased, and systems generally ran more smoothly than in prior quarters.

With one exception — Nordic Aqua Partners — all land-based producers posted wider operating losses in Q3-2025. NOAP did improve year-over-year, but even with excellent biology and increasing harvest volumes, they still reported a significant negative EBIT. The underlying pattern remains: improved biological performance alone is not enough to overcome the structural cost base in land-based salmon farming, especially when prices fall.

On the surface, the explanation seemed obvious: global salmon prices were weak. But as I dug into the data, something else jumped out — a deeper structural issue that Q3 made impossible to ignore.

The problem isn’t just price. It’s the way we talk about costs.

For years, the land-based sector has leaned heavily on EBITDA per kilo as its preferred performance metric. (Earnings Before Interest, Taxes, Depreciation and Amortization) Investor decks show clean upward trajectories: negative EBITDA in the construction phase, breakeven EBITDA two or three years after first harvest, and positive EBITDA shortly thereafter. The implied message is simple:

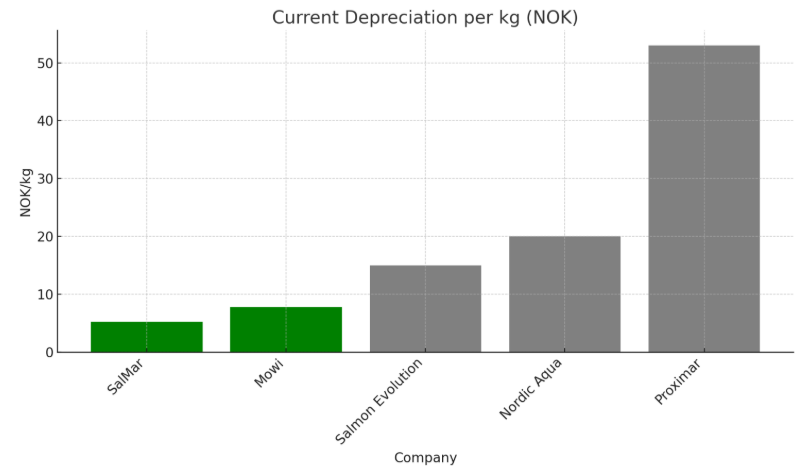

Current depreciation per investor reports

“Once EBITDA improves, EBIT will follow.”

In other words, the losses are temporary; scale will fix everything.

This belief is not accidental — it’s inherited from net-pen salmon farming, where depreciation per kilo is tiny and EBITDA is a perfectly reasonable shorthand for operating earnings. In the marine sector, depreciation is so small — 5 to 8 NOK/kg for companies like SalMar and Mowi — that EBITDA and EBIT are often only a few NOK apart. In that context, it actually is reasonable to treat EBITDA as a meaningful proxy for profitability.

But land-based farms are an entirely different animal.

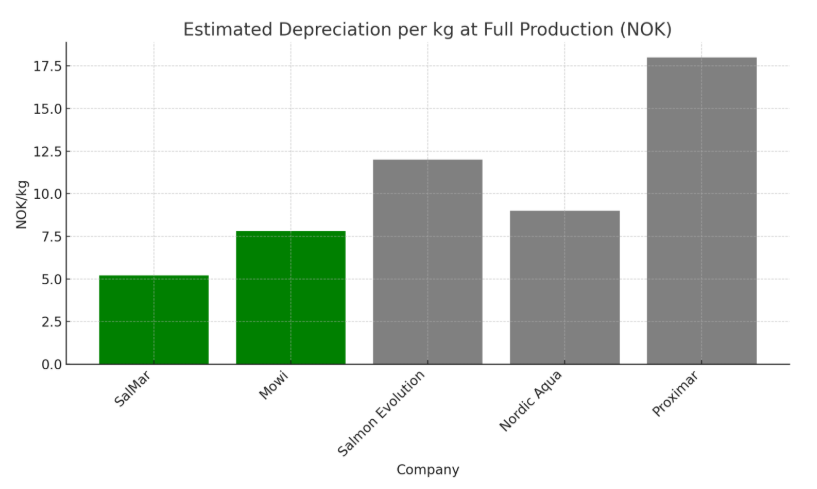

Depreciation levels assuming production goals and budgets are realized.

RAS is not a net-pen with a roof — it is a profoundly different production system.

A modern recirculating aquaculture system (RAS) is heavily reliant on high-pressure recirculation pumps, degassers, CO₂ strippers, ozone and UV sterilization, membrane filters, massive HVAC and temperature-control systems, complex biofilters, oxygenation arrays, backup power and redundancies, thousands of meters of pressurized pipe, sensors and SCADA control systems. (Flow-through systems are spared some, but not all of this complexity)

Many RAS components have short useful lives — often 7–12 years — and may operate 24 hours a day, under constant load, in warm, corrosive, oxygen-rich environments.

Civil works (concrete tanks, foundations) may last decades. But the heart of a RAS facility — the machinery that keeps the fish alive — does not.

This is why depreciation per kg is so dramatically higher in land-based systems:

– SalMar: ~5 NOK/kg (net pen producer for comparison)

– Mowi: ~8 NOK/kg (net pen producer for comparison)

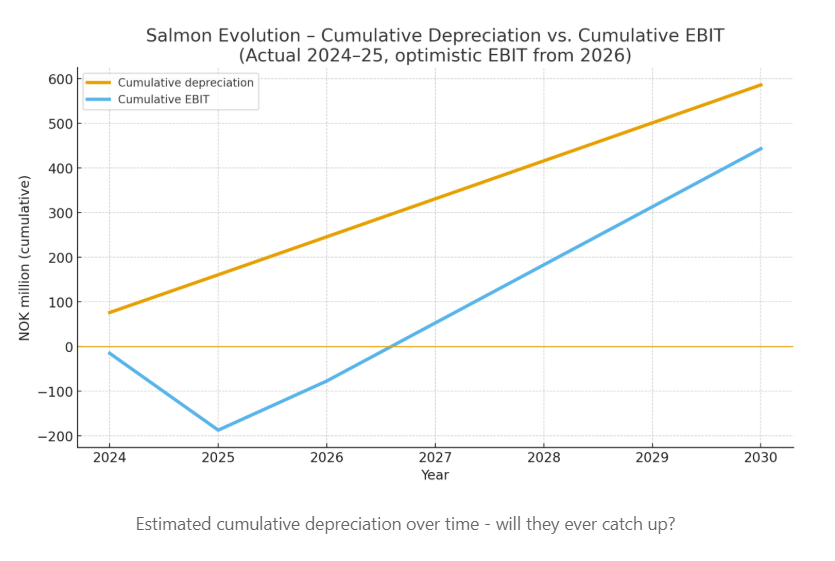

– Salmon Evolution: ~15 NOK/kg

– Nordic Aqua Partners: ~20 NOK/kg

– Proximar: ~53 NOK/kg

These are not rounding errors. They are not “accounting artifacts.” They are the economic cost of replacing the machinery that keeps the system functioning.

And the clock starts ticking from day one.

Why Q3-2025 was so revealing

In Q3-2025, Salmon Evolution, Nordic Aqua, and Proximar all reported improving biology, higher biomass, more stable operations, and larger harvests.

And yet:

– EBIT losses widened

– EBITDA losses persisted

– operating cash flow tightened

– financing needs increased

The reason is straightforward:

EBIT didn’t improve because depreciation didn’t improve.

And depreciation didn’t improve because the assets are aging, even as farms are still in their ramp-up period.

RAS companies are trying to reach profitability on systems that are already halfway to their first major replacement cycle.

That is a very different dynamic from net-pen farming, where assets are cheap, long-lived, and modular.

Why early investors are living on borrowed time

This is the part most investors don’t fully appreciate.

A land-based salmon farm typically requires 3–4 years from groundbreaking to first harvest, and then another 2–3 years to reach full capacity. By the time EBITDA approaches breakeven:

– pumps are 5–7 years old

– membranes have been replaced multiple times

– chillers and heat pumps have significant wear

– oxygen and recirc systems are entering mid-life

– controls and sensors require renewal

– tank liners are approaching replacement cycles

In other words:

The assets are aging faster than the ramp-up schedule.

Early-stage investors therefore rely on a very narrow window:

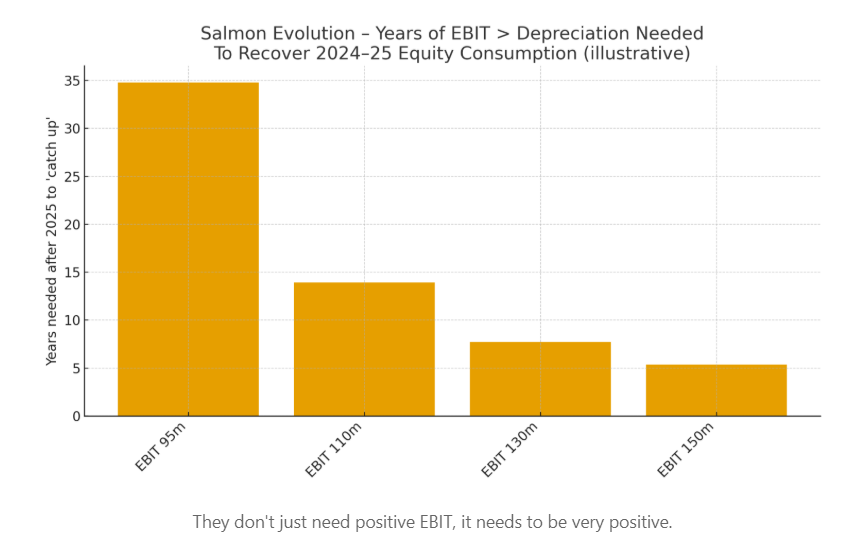

Years 4–7 must produce strong EBIT — or there will never be a return.

If EBIT does not exceed depreciation by the time the plant is fully stocked, the company:

1. cannot pay dividends

2. cannot build reserves for future capex

3. cannot service debt efficiently

4. cannot refinance cheaply

5. cannot justify a high exit valuation

Instead, the company must:

– raise new equity (down-round)

– increase borrowing (at higher rates)

– or allow systems to degrade — which in RAS leads directly to biological failure

This is exactly what happened with Atlantic Sapphire. After seven years of continuous investment and mounting breakages, they needed USD 60 million just to maintain operations and keep fish alive — a raise that came with massive dilution and heavy losses for early shareholders.

The capex doesn’t go away. It simply waits.

“Cash-positive” is not a business model — it is a countdown clock

One of the most common investor lines in RAS is:

“We’re cash-positive now, EBITDA is improving, EBIT will follow.”

But if EBIT does not eventually exceed depreciation and bank enough capital to fund the first major replacement cycle, then the business is:

– eroding its asset base

– consuming its own balance sheet

– deferring inevitable capex

– building future cash obligations

– and providing no economic return to equity holders

– while asset lives shorten

A pension fund cannot pay pensions from EBITDA. A private equity firm cannot sell a company at a multiple of EBITDA if EBIT is negative. A strategic buyer will not acquire a facility that cannot fund its own replacement cycles.

Ultimately:

A land-based salmon farm that cannot beat depreciation is not a profitable enterprise — it is a slow liquidation of investor capital.

And that is why Q3-2025 matters so much: The numbers are finally making that reality unavoidable.

Conclusion: The industry needs to stop pretending EBITDA is enough

Net-pen farmers can use EBITDA because their depreciation is tiny and their assets last decades.

Land-based salmon farms cannot use the same playbook. Their economics are dominated by:

– high capex per kg

– rapid equipment aging

– short asset lives

– high maintenance cycles

– expensive reinvestment

– and large depreciation charges that reflect real economic cost

If investors and operators continue to use EBITDA as a proxy for profitability, they will continue to misunderstand the true viability of these systems — and will continue to be surprised when early investors are wiped out, facilities need emergency funding, and economics never meet expectations.

If you made it this far, I salute you. Comments and feedback welcome.